The Ultimate Tax Filing Guide for American Liquor Stores 2026

Running a liquor store in the U.S. means dealing with more tax complexity than most retail businesses and not because liquor store owners are doing anything wrong.

Liquor stores operate at the intersection of retail sales tax, alcohol regulation, and inventory-heavy operations. Small missteps—like incorrect POS tax setup, missed distributor credits, or poor inventory tracking—can quietly compound until tax filing season becomes stressful, expensive, or risky.

This 2026 guide is written for real operators:

- single-location liquor stores, and

- growing, multi-location businesses

It explains what actually matters, how taxes differ by state, and how to build a simple system that makes filing predictable instead of painful.

Also Read: 2026 Tex Deadlines You Can't Afford to Miss

Why Liquor Store Taxes Feel Harder Than Other Retail

Liquor stores don’t fail tax audits because of fraud.

They fail because of inconsistency.

Compared to typical retail, liquor stores face:

- higher transaction volume

- stricter regulation

- more audits and notices

- heavier reliance on distributors

- tighter margins tied to inventory accuracy

The stores that stay compliant aren’t “better at accounting.” They simply run monthly routines that don’t break.

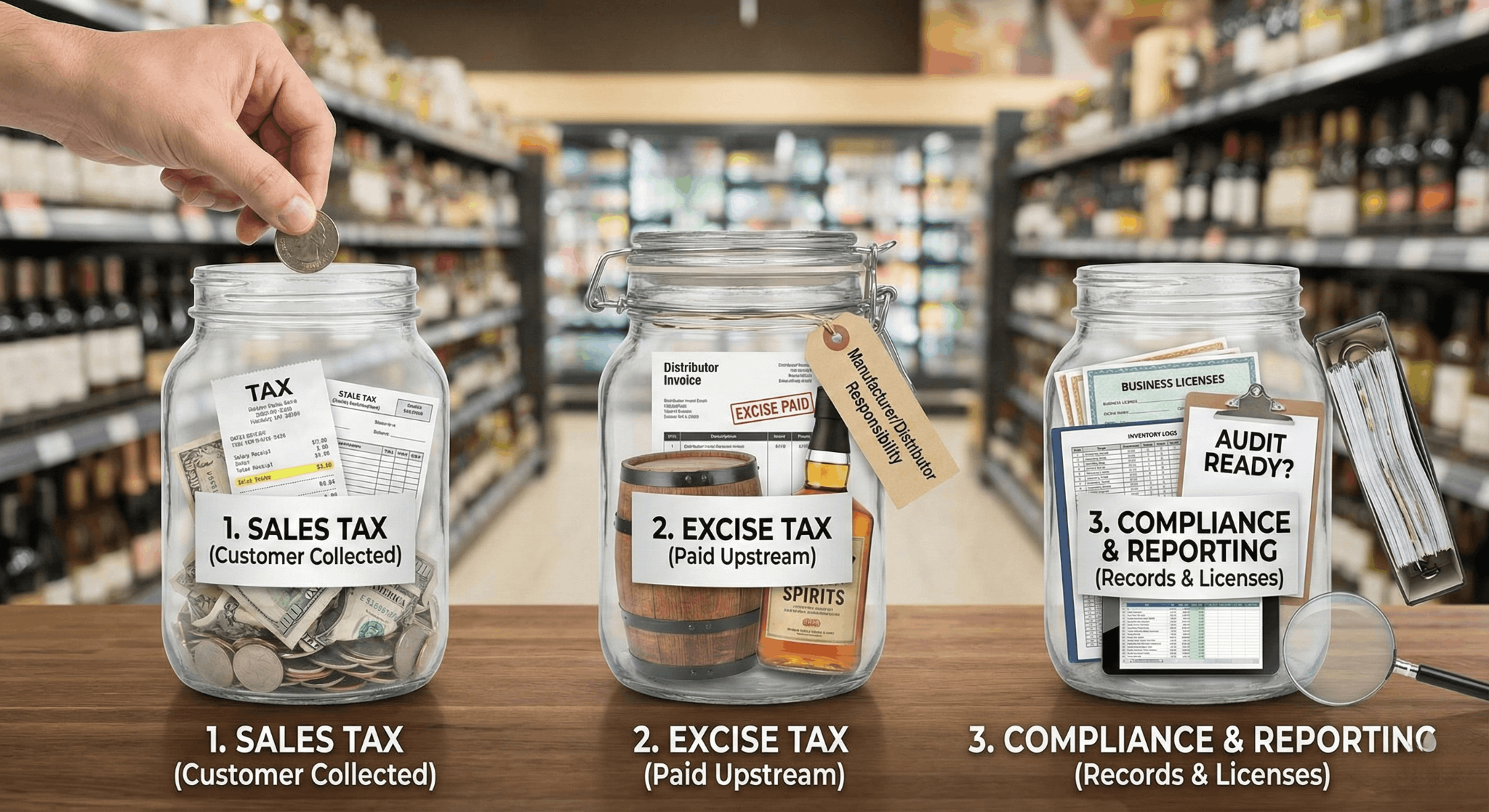

Understanding the Three Taxes Liquor Stores Deal With

Before getting state-specific, it helps to separate liquor store taxes into three buckets.

1. Sales Tax (Your Primary Responsibility)

Sales tax is collected from customers and remitted to the state (and sometimes cities or counties). This is where most liquor store issues happen—because item-level rules matter.

2. Excise Tax (Usually Paid Upstream)

Alcohol excise taxes are typically paid by manufacturers, importers, or distributors. Most liquor stores do not file federal excise tax returns, but they must still maintain clean receiving and inventory records.

3. Compliance & Reporting

Licenses, distributor invoices, inventory movement, and sales records all feed into your tax posture. Even if you don’t owe excise tax directly, sloppy records create problems fast.

Sales Tax Basics for Liquor Stores (2026)

Sales tax rules vary by state, but liquor stores share a common risk:

taxability depends on what you sell, not just where you sell it.

Most errors come from:

- POS items mapped to the wrong tax category

- refunds or voids not reducing taxable sales correctly

- discounts applied incorrectly

- deposits and processor fees confusing reconciliation

A simple rule to remember:

Your POS sales, tax collected, and bank deposits should reconcile every month.

If they don’t, fix it immediately—don’t wait until filing.

What’s Taxable? A State-by-State Reality Check

(Alcohol + Non-Alcohol Items)

Below are real-world patterns, not legal fine print. Always confirm edge cases locally.

California

In California, packaged beer, wine, and spirits sold in liquor stores are generally taxable. Most non-alcohol items—snacks, mixers, soda—are also taxable.

What often causes confusion is the CRV bottle deposit, which is reported separately and should not be treated as normal taxable sales.

California liquor stores also deal with layered district taxes, making correct POS setup critical.

Texas

Texas treats packaged alcohol as taxable, but food items can be exempt depending on how they’re classified.

Mixers, accessories, and non-food items are typically taxable. Local tax caps and discount handling often trip stores up—especially when promotions are run without reviewing tax logic.

Florida

Florida taxes packaged alcohol, but many grocery-type foods are exempt. Candy, soft drinks, and accessories are taxable.

Liquor stores in Florida get hit hardest by late filings, since penalties apply quickly after the 20th of the following month.

New York

New York taxes packaged alcohol but exempts many food items sold for off-premise consumption. Prepared items and accessories remain taxable.

The challenge in New York is item-level accuracy and managing assigned filing frequencies, which can change as volume grows.

Illinois

Illinois taxes packaged alcohol and applies different treatment to grocery items versus candy, soda, and accessories.

Liquor stores here must also watch for accelerated payment schedules, which compress deadlines and increase compliance pressure.

Excise Tax: What Liquor Stores Need to Know (Without Overthinking It)

Most liquor stores don’t file excise tax returns—but excise tax still affects you.

It’s typically embedded in:

- distributor pricing

- category margins (beer vs wine vs spirits)

When audits happen, regulators don’t ask, “Did you file excise tax?”

They ask:

“Show us what you received, what you sold, and what’s left.”

That’s why distributor invoices, credits, and inventory movement matter more than the tax form itself.

2026 Sales Tax Filing Calendars (Operator View)

Forget legal calendars. This is how operators actually stay compliant.

California

Most monthly filers submit by the last day of the following month.

Best practice: close books by the 10th, file by the 20th.

Texas

Monthly returns are due on the 20th.

Treat the 15th as your internal deadline.

Florida

Returns are due on the 1st and late after the 20th.

File early—penalties come fast.

New York

Returns are due 20 days after the period ends.

Plan your close within the first 10 days.

Illinois

Returns are due on the 20th.

Watch for notices that move you to accelerated schedules.

Universal rule: Even if you file quarterly, reconcile monthly.

Single-Store vs Multi-Location: Where the Line Is Drawn

Single-Store Liquor Shops

You can stay lean if:

- POS tax setup is correct

- deposits are reconciled monthly

- inventory is checked regularly

- distributor invoices are organized

Your biggest risk is relying on memory instead of systems.

Multi-Location Liquor Stores

Once you add locations, inconsistency becomes your enemy.

What changes:

- more tax jurisdictions

- more inventory movement

- more staff touching the process

What becomes mandatory:

- standardized POS tax rules

- centralized accounting

- a shared close calendar

- store-level receiving discipline

Multi-location tax problems almost always come from setup drift, not intent.

The Liquor Store Monthly Close Kit (Why It Matters)

The simplest way to reduce tax stress is to stop treating filing as a one-time event.

A Monthly Close Kit brings everything together in one place:

- POS sales & tax summaries

- bank deposits and processing fees

- distributor invoices and credits

- inventory movement and shrink notes

- filing status and exceptions

For single stores, this can be owner-managed. For multi-location businesses, each store contributes and HQ consolidates. This turns tax prep into review, not investigation.

Filing With a CPA vs Without One

With a CPA

A CPA is most valuable when:

- your data is already clean

- inventory is accurate

- sales tax exposure is visible

They should be optimizing structure and defending risk—not fixing messy books.

Without a CPA

Possible for very small stores—but risk increases fast as volume grows.

If you have:

- multiple locations

- frequent notices

- large inventory swings

a CPA quickly becomes cheaper than penalties and rework.

How Tax Strategy Changes as You Grow

- Small single store: focus on accuracy and deadlines

- High-volume store: add weekly deposit checks and shrink reviews

- Multi-location: standardize everything early

Growth doesn’t just increase workload—it increases audit exposure.

Final Takeaways for Liquor Store Operators for 2026 Tax Filing

Liquor store taxes aren’t complicated. They’re unforgiving of inconsistency.

The strongest operators:

- reconcile monthly, even if they file quarterly

- understand how excise tax flows through pricing

- keep inventory and invoices clean

- standardize early when scaling

Taxes stop being stressful when they become routine.

Sahana is a seasoned GTM leader with a passion for building startups. She excels in crafting GTM strategies for tech products, driving revenue growth.